Web3 and insurance

What will earn revenue and how

Five months after my post about why bankers should pay attention to metaverse, we are now seeing banking as a high potential usecase in McKinsey’s June 2022 Value Creation in the metaverse report. Five months after mentioning light weight glassess are yet to be invented, we are seeing China’s 6G plans1 heavily focussed on AR glasses.

So, here’s an attempt to hold out and look at new business for insurance in Web3.

Insurance is a high income, high trust, but low touch point financial services product that’s more fiercely regulated than banking products and negotiable instruments. It is non optional for B2B usecases, and even so non negotiable when your organisation offers life or medical insurance with limited riders at extra costs. Tax saving instrument or plan linked insurance products, auto insurance and renewals are also largely driven more by external agency than individual’s limited choices. What drives revenues - new incremental business, lesser claims and more renewals. So how do we see insurance value chain and products evolve in promise of individual ownership aka Web3? Will individuals want to saunter in metaverse to buy traditional insurance in the metaverse or for the metaverse objects, digital assets and new asset classes? Who will provide insurances for digital avatars, gaming skins and coverage against smart contract failure that didn’t apply security features in the code?

Several insurance companies are entering the space with innovative ideas right when embedded finance started eating up regular insurance chains of bancassurance and agency models. Lemonade’s partnership to provide blockchain based weather insurance to farmers is a low denomination, smart contract based insurance. The contract pays the claim amount with rules evaluated based on third party data sources (oracles). Blockchain is not new and most financial services tried proof of concepts, usecases in 2015-18. What has changed now is maturity of objects, applications and communities building it into trillions of dollars economy (tip of hat to Cardano’s CEO’s speech about crypto currency). Further, digital assets presents a massive $800 trillion economy in public market itself. Evertas is one of the early digital-asset insurance companies based in the US. They provide coverage for digital asset holders and businesses, including custodians, exchanges, traditional financial institutions, high-net-worth individuals, family offices, and market utilities.

Insuring Web 3

The Web3 economy is currently under-insured and has huge potential for future growth. Today, out of $1 trillion in crypto assets, less than 1% are insured.2 Insuring the Web3-related assets such as digital currencies, NFTs, and liabilities (business liabilities, professional risks and liabilities ) is vital. The new iteration of the Internet has more lawyers and accountants interested in legal, governance and protection, treatment of assets on books as much as technologists and blockchain developers. Smart contracts are the beating heart of Web 3 as quoted by Kary Bheemaiah. And these lines of code do the most heavy lifting of value. One of our Web3 experts, Kai Libicher, had penned3 - there’s barely any insurance for bugs and hacks in Web3 protocols, stablecoins that lose their pegs, funds get hacked and lost private keys that cost billions of dollars already.

What is the scope of insurable Web3 risks?

Theft insurance against for crypto exchange is tricky because of technical risks rather than understanding new features of smart contracts, security checks across emerging bridges and security designs of smart contract. This space will evolve as several countries from Germany, Japan, UAE, Norway, Australia, Singapore, UK and the US are building their regulations around stablecoins, cryptocurrency. There are several large organisations holding cryptocurrencies on their balance sheets and wide range of companies have exposure to Web3-related risks. Insuring stablecoins, crypto-assets, CBDCs, decentralised finance collaterals, NFTs and a host of companies of the Web3 stacks and exchanges also need professional liability, property and health insurance.

New build and propositions for insurance

Rules engine with automated triggered (smart contracts) make it easier to customise policies, data feeds (oracles) with data feeds or even IoT sensor data over fast connectivity can help in automating claims and reducing percentage of time to payout, distributed decentralised apps (dApps) and governance, utility (tokens) structurally changes zero-based budgeting of a company to first investing and understanding new tech with new cost structures. Smart contract education for product distributors and customers is important as they are not transparent. SaaS cost of API links to data oracles needs to be considered as accuracy of data is more critical than ever. Pricing accuracy of products and underwriting can benefit from the same oracles combined with existing data feeds. Insurers must build the capability and new roles to participate in the new insurance structures.

Case study - Etherisc

Etherisc, for example, is a non profit that partners with other ecosystem players to offer a range of Web3-based insurance products, including crop insurance, hurricane insurance, flight delay insurance, and digital wallet cover. Most elements are decentralised via blockchain. Products such as Collateral Protection for Crypto-backed Loans are under design by community. The policy pays up to 100% of the issued loan amount if value of collateral provided by the borrower (i.e. ETH, or tokenized car) drops by 90% or more.

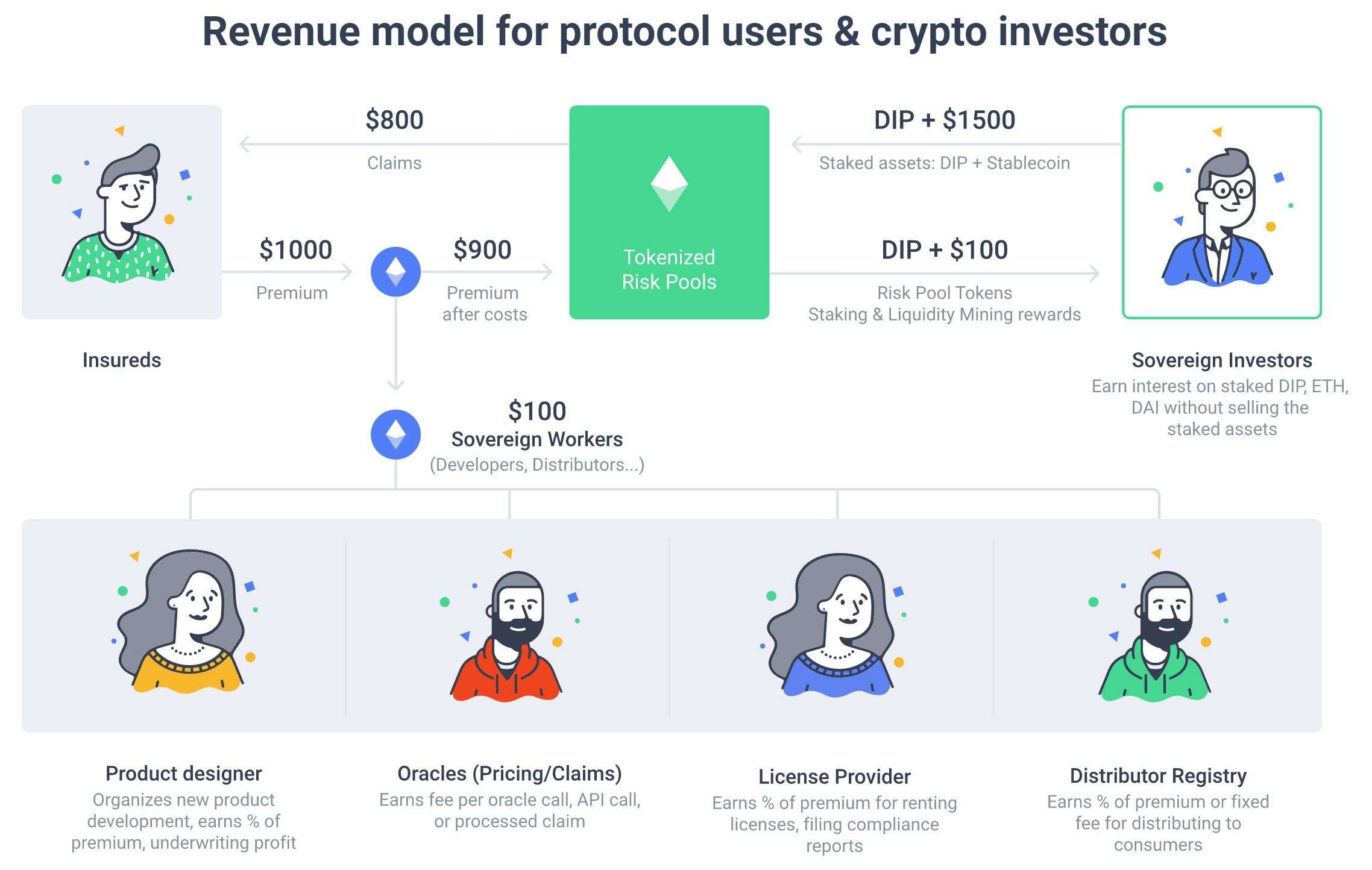

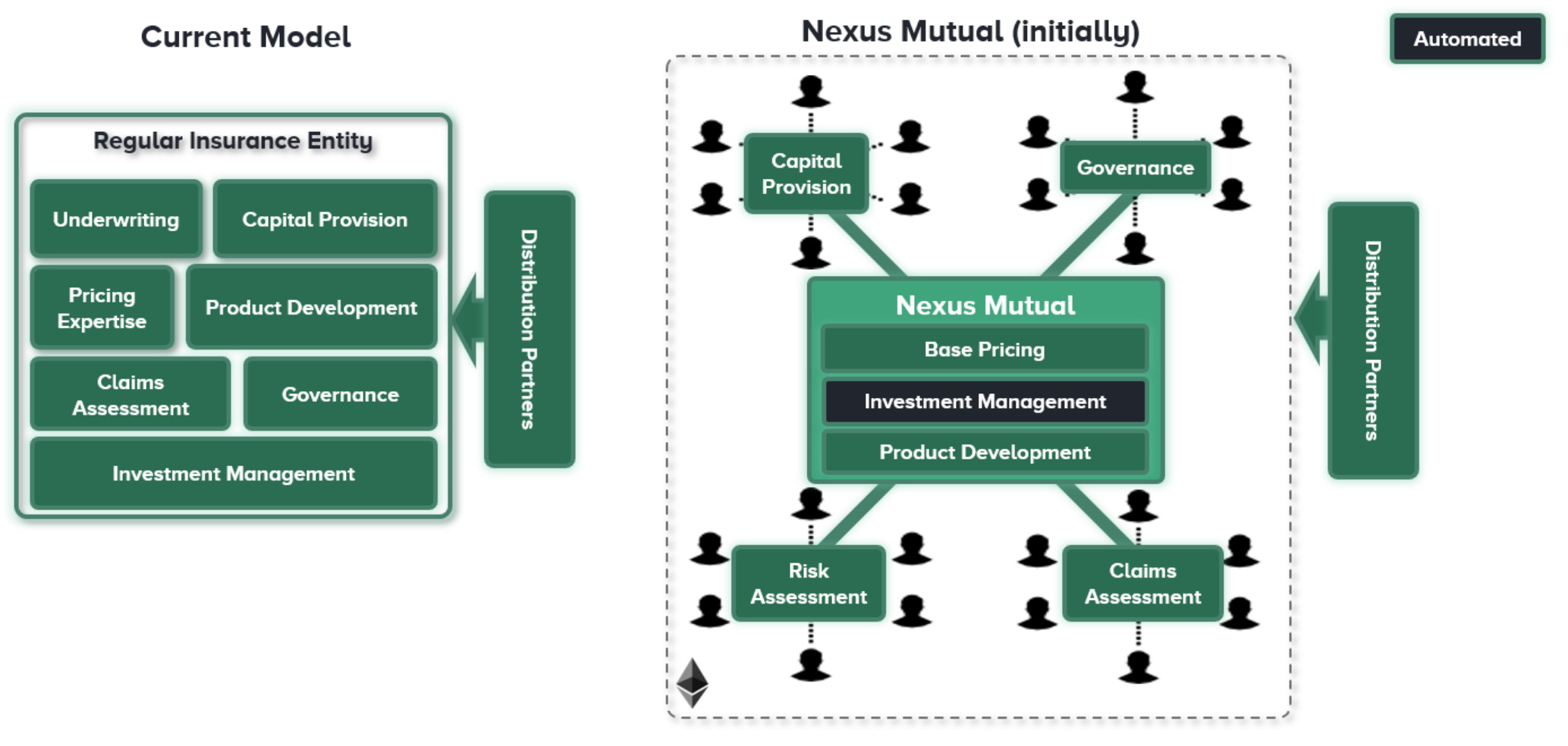

Case study - Nexus Mutual

Nexus Mutual4 is a blockchain-based “mutual” that offers decentralized insurance products for digital asset holders. Pricing, claims, investments are decentralised whereas products and governance is partially centralised.

Nexus Mutual members hold NXM tokens (ERC-20 token), which allows them to vote on claims assessment and governance issues. They can also become risk assessors and earn rewards by staking their tokens (essentially, contributing tokens to a pool that is used when a payout occurs). Incentive structures need more resilience against game theory attacks and these are overlaid with timing windows and human intervention to avoid extreme situations.

Imperatives for insurers

Insurtech mostly succeeds at scale in the form of B2B distribution with incumbents. In case of Web3 insurance propositions and distribution, structural success depends lesser on traditional players. Thus, what is the ambition in near term and mid-term?

Which are the potential customers and high business impact usecases? How do people really use metaverse and digital assets and how should insurance engage with the Web3 users and ecosystem? What are the calculated risks and investments in building capabilities and partnerships to assess risk?

It’s June 2022 and Goldman Sachs is ready to buy Celsius’ assets. Clearly, with over $120 Bn investments in metaverse alone in H1 2022, we are far from winter. Even if we still take a regulatory view that decentralised or autonomous organisations are not the best yet, Harvard Business Review has written ample about both Why must one build in Web3 and DAOs and WEF has recently published a report on DAO. Some people have started listing their roles in DAOs are official positions in their LinkedIn profile (even as LinkedIn has started pulling down avatar like photos while Microsoft continues to build in Web3). Stemming from distrust, privacy concerns and regular hacks in Web3, regulations get center-stage before innovation unsurprisingly and we may first have to achieve Web2.5 before jumping onto Web3 or Jack Dorsey’s Web5. With a deluge of reports, it may feel like jumping on a running train, but it felt the same in 1800s as well. Identifying business relevant usecases and exploring new ideas has probably stood the test of time.

China just killed Meta’s metaverse:

www.coindesk.com/markets/2018/11/21/the-crypto-insurance-market-may-total-6-billion-thats-nowhere-near-enough/

What they don’t tell you about the metaverse - Kai Libicher https://www.linkedin.com/pulse/what-dont-tell-you-metaverse-22-kai-libicher/

https://nexusmutual.io/